What’s going on with my mortgage costs?

In December, the Bank of England (BoE) announced the ninth consecutive increase to the BoE “bank” rate (also often referred to as the “base” rate).

Why does the BoE rate matter?

The BoE base rate influences most other savings and borrowing rates across the British banking system, and is particularly important in the area of mortgage borrowing.

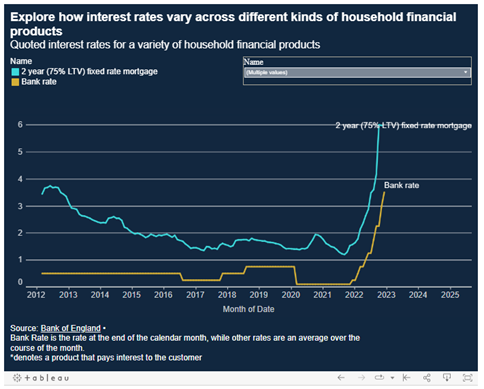

Typically, when the bank rate increases, so do mortgage rates offered to the UK population. This relationship can be seen in this image taken directly from the BoE website:

The difference between the yellow line (representing the BoE base rate) and the blue line (representing a typical two-year fixed mortgage rate) is to allow for the risks taken by your lender, the costs of offering and promoting the product, and of course for their profit (or margin) also.

What does this mean for my mortgage?

Any change to the BoE rate has an almost immediate impact on the costs of borrowing for those on variable rate or tracker mortgages.

Over time, it also has an impact on all those coming to the end of an existing “fixed rate” mortgage period. Many such households in this position will find a very sharp increase in their mortgage interest rates when their current fixed term ends, with some jumping from (say) a 2% rate to the current average of around 6%. This is likely to be adding several hundred pounds to the monthly mortgage costs for many borrowers.

Historical comparisons?

However, there are still those – including some from within the mortgage industry – who continue to suggest that this is not a major concern. Many commentators reference the BoE rates of the late 1980s and early 1990s which were far higher than those being experienced today. Yet that simple analogy is dangerously flawed. Interest rates were indeed very much higher last century, but conversely, the amount of debt per household was significantly lower.

The ultra-low interest-rate environment that the UK has experienced since the 2008 Credit Crunch has led to a supply of “cheap” finance, which in turn has fuelled an already expensive housing market. The result is that whilst interest rates have been exceptionally low, the total value of mortgage debt is far, far higher than it has been in the past.

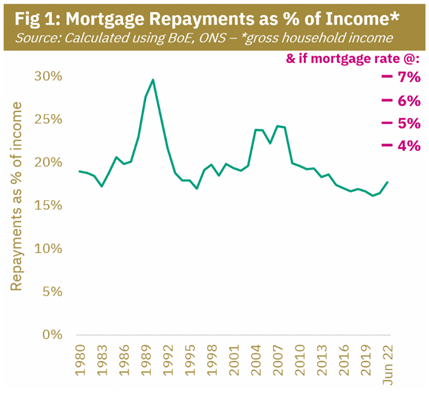

It follows that even relatively small increases in interest rates will have a far bigger impact on household finances than it would in, say, 2007. This chart from BuiltPlace demonstrates the level of mortgage repayments as a percentage of income if mortgage rates were at 4%, 5%, 6% or 7%. You will note using the current average rate of around 6% for example is the highest mortgage burden since the early 1990s.

Don’t panic!

So, mortgage costs are likely to increase for many – perhaps most – borrowers in 2023, and will place a new strain on many household budgets.

That is of course worrying, but please don’t panic.

Borrowers today have far more support and consumer protections now than was the case in the 1990s, and there are usually several viable options to consider if you feel that you can’t afford your new level of mortgage repayments at this time.

With this in mind, we would encourage you to first review the “Four steps to financial health” videos here on the Financial Wellbeing Hub. In particular video 3, “Managing Debt”, will help you better understand your options.

If you still feel that you are struggling to make your repayments, then it’s a good idea to make contact with your mortgage lender so that they can explain all the options available to you. Other support options are also listed in the above video.

This document is provided for information only and is correct at the time of writing (05/01/2023). Links to websites do not indicate any endorsement of that website or service by Partners&.