The government and banking industry agree on more flexibility for mortgage holders as interest rates increase again.

The 13th successive increase in the Bank of England’s base rate has sparked panic for many working people with mortgages, and in particular those approaching the end of their current fixed-term mortgage deal.

The problem:

This level of concern is entirely understandable.

Many 2-year fixed-term deals were agreed during the pandemic when the base rate was at a 300-year historic low. This has resulted in many existing mortgage deals being fixed at (or around) a 2% interest repayment rate.

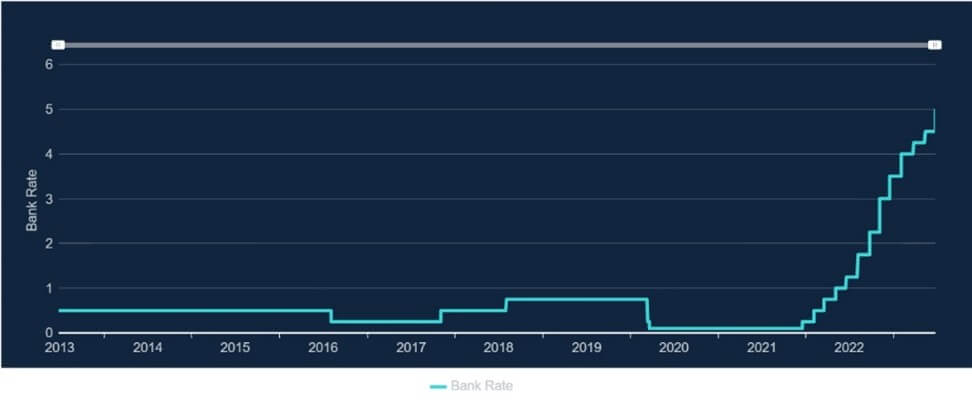

But since the end of 2021, the Bank of England has been seeking to control inflation by increasing its base rate. There have been 13 increases in the base rate since December 2021, and last week the rate was increased to 5% (see the chart below from the Bank of England’s website):

Where are we now?

In anticipation of the increase last week, the mortgage providers (typically Banks and Building Societies) increased their typical two-year fixed-term mortgage rates to 6% or over.

Whilst historically this is not a high rate, it will still represent a very significant leap in monthly mortgage repayment costs for hundreds of thousands of households when their current fixed-term deal ends. This problem is compounded by the ongoing cost-of-living crisis that households are currently experiencing.

New support agreed

This is why the government have met with mortgage providers to agree on new flexibilities to support those households struggling to make their mortgage payments.

The lenders – which cover over 75% of the market – agreed to a new mortgage charter providing support to residential mortgage customers.

The charter includes (the text below is taken directly from the government website):

- Anyone worried about their mortgage repayments can call their lender for information and support, without any impact on their credit score and we would encourage you to contact your bank who are there to help.

- Customers won’t be forced to have their homes repossessed within 12 months from their first missed payment.

- Customers approaching the end of a fixed rate deal will be offered the chance to lock in a deal up to six months ahead. They will also be able to apply for a better deal right up until their new term starts, if one is available.

- A new agreement between lenders, the FCA and the government permitting customers to switch to an interest-only mortgage for six months, or extend their mortgage term to reduce their monthly payments and switch back to their original term within the first six months, if they choose to. Both options can be taken without a new affordability check or affecting their credit score.

- Support for customers who are up to date with payments to switch to a new mortgage deal at the end of their existing fixed rate deal without another affordability check.

- Providing well-timed information to help customers plan ahead should their current rate be due to end.

- Offer tailored support for anyone struggling and deploy highly trained staff to help customers. This could mean extending their term to reduce their payments, offering a switch to interest only payments, but also a range of other options like a temporary payment deferral or part interest-part repayment. The right option will depend on the customer’s circumstances.

Thoughts and what now?

These new flexibilities are very welcome and will help some households reduce the scale of their monthly mortgage costs.

It is however important to note that you don’t need to make this decision without support.

Indeed The Chancellor has made it clear that;

“absolutely anyone can talk to their bank or their mortgage lender and it will have no impact whatsoever on their credit score”

So if you feel that your household may need to access this enhanced level of support, then speak to your provider as soon as possible.

It is also worth noting that your existing provider may not always be offering the best remortgage deals. So it is worth shopping around, and specialist, whole-of-market, mortgage providers sometimes have access to deals that may not be otherwise available to your household.

Don’t panic!

Lastly, and certainly not least, please don’t panic.

It is often a good idea to get some expert support in such situations, and there are plenty of free-to-access support options available. We have listed some of the main options in this article already available on the Financial Wellbeing Hub.

Got a question? Want to know more?

Contact our expert